The good, bad and ugly, according to JPMorgan

Robin Wigglesworth AUGUST 18 2023

The biggest question in global macroeconomics at the moment is whether China is on the cusp of a “balance sheet recession”. This sexy bit of economic jargon was first coined by Nomura’s Richard Koo to describe Japan’s lost decade(s), but is most commonly known as “Japanification”.

It can be described simply as a protracted period of deflation, economic sluggishness, property market declines and financial stress as households/companies/governments unsuccessfully try to deleverage after a debt binge.

Earlier this month, JPMorgan analysts Haibin Zhu, Grace Ng, Tingting Ge and Ji Yan published a fascinating deep-dive into the subject, which we have finally digested. The tl;dr is that JPMorgan’s economists see some spooky similarities between China today and Japan in the 1990s, but “enough differences to suggest the ‘balance sheet recession’ diagnosis, and policy recommendations that flow from it, is/are not correct”.

That said, there are some aspects they highlight that actually look worse in China (a lot worse in some cases), so let’s dive in.

The bad

Any fan of 1990s Dad Thrillers will remember Rising Sun, a film based on a book by Michael Crighton and starring Sean Connery and Wesley Snipes (it doesn’t get much more 90s than that). The subplot was America’s anxiety over Japan’s seemingly irresistible rise, which seems quaint in today’s eyes, but also very reminiscent about modern US angst over China.

Sadly, JPMorgan doesn’t explore cinematic history in its report but notes that there are a few eerie other similarities between China’s current predicament and Japan’s in the early 90s.

First is similarity in housing market development. As we have argued, China’s housing market correction since 2021 is not only cyclical (or policy-induced), it is also structural reflecting major changes in demand vs. supply in the housing market. This is similar to Japan’s housing market correction in the 1990s.

Second is similarity in financial imbalance, i.e. the pace of increase and level of debt problem. According to the BIS, China’s total non-financial credit/GDP ratio approached 297% of GDP by end-2022, similar to Japan in the 1990s. Also similarly, debt is mainly domestic and domestic saving rate is high in both countries.

The problem of population aging is also similar. The share of aged population (65 and above) was 12.7% in 1991 in Japan, similar to China in 2019 (12.6%).

On the external front, Japan’s large trade surplus vs. the US led to trade conflict, as exemplified in the Plaza Accord in 1985 (5-6 years before the start of Japan’s lost decade) and US-China tariff war that started in 2018. From a broader perspective, the rise of Japan (30 years ago) and China (right now) to challenge the status of the US as the largest economy in the world is quite similar, leading to the fight-back from the US that initially focuses on reducing the bilateral trade imbalance.

The good

But there are some important differences as well (aside from the lack of a China-focused Snipes movie). Some of these differences are actually worse in China’s case, and some are better.

Let’s look at what JPMorgan thinks are the “good” differences, before turning to the ugly. First of them (and JPMorgan reckons perhaps the most important difference) is a much lower urbanisation ratio in China.

China’s urbanization ratio was 65% in 2022, and if excluding migrant workers who live in urban areas but do not have the same privileges as urban citizens, the hukou ratio was only 47%. In Japan, urbanization ratio exceeded 77% in 1988. Lower urbanization ratio points at larger potential for productivity increase associated with labor migration from agricultural to non-agricultural sectors. In the housing market, it suggests that China may have huge replacement demand for housing in the so-called new urbanization process, i.e. when non-hukou urban residents are granted hukou privileges and need to replace their rural area homes with urban-area apartments. The current gap of 18% of total population between urban population and hukou population implies potential housing demand from a maximum of 250 million people, or 100 million families.

Second, China has a much larger domestic market, a larger pool of STEM graduates and comprehensive manufacturing sectors. While China may be facing a more challenging external environment than Japan in the 1990s, there is also hope that China can achieve technology upgrade and commercialization in some areas. For instance, China has become a leading player in new energy and new energy vehicles in recent years.

Third, perhaps somewhat debatably, we think China’s housing price overvaluation is less severe than Japan in the 1990s. This is in part due to prolonged administrative control on new home prices and in part due to solid income growth. Our estimates show that housing affordability has continued to be a big problem in tier-1 cities: it took 21.1 years of household income to buy a 90-sqm apartment in 2010, and 16.6 years of household income in 2022. By contrast, housing affordability is much better in tier-2 and tier-3 cities that account for the majority of China’s housing market. Using the same house price/income measure, the ratio fell from 13.4 in 2010 to 8.3 in 2022 in tier-2 cities, and from 10.2 in 2010 to 6.1 in 2022 in tier-3 cities.

Fourth, China’s capital account is not fully liberalized. This will reduce the risk of fire sale of domestic assets (mainly housing) to invest overseas. In fact, many households still choose to hold multiple homes amid housing market corrections, because house price decline has been modest due to government control and, in addition, there are limited options for alternative investment.

Lastly, the Chinese government has stronger control of both asset and liability sides of the debt problem. This could be a double-edge sword: it implies that the probability of a sudden-stop debt crisis is smaller in China, but the zombie parts of the economy will continue to stay and likely further expand, intensifying the moral hazard problem and weakening incentives for structural reforms. This may crowd out more productive activities in the economy and lead to faster-than-expected slowdown in economic growth.

So, less urbanisation; a less extreme property bubble; capital controls and many government policy levers that can still be pushed and pulled. Which are all admittedly pretty major differences.

Unfortunately for China, it differs from 1990s Japan in some . . . suboptimal ways.

The ugly

JPMorgan’s main concern is that China is actually ageing more rapidly than Japan was, which has led to predictions that it will ‘grow old before it grows rich’ — a kind of demographics-caused middle-income trap.

In Japan’s case, the share of population aged 65 and above exceeded 10% in 1983, and exceeded 14% in 1994. The birth rate fell from 12.7 (per 1000 people) to 10.0 during that period. In China’s case, it took only 7 years (from 2014 to 2021) for the 65 plus population to increase from 10% to 14% of total population, and the birth rate has fallen faster from 13.8 (per 1000 people) to 7.5 during that period (and further down to 6.77 in 2022, similar to Japan in 2020 at 6.80). In addition, China’s total population started to decline in 2022, while Japan’s total population started to decline in 2008, nearly two decades after the start of the lost decade.

Second, China’s GDP per capita was around US$12,800 in 2022, much lower than Japan in 1991 at US$29,470. While lower GDP per capita may imply higher growth potential, it suggests that China is becoming old and high-indebted before it becomes rich.

The accompanying chart is pretty stark:

Moreover, JPMorgan’s economists also point out that the global economic backdrop is worse for China than it was for Japan in the 1990s, and thinks the Chinese government has less scope for stimulative fiscal measures than is commonly assumed:

. . . The external environment is more challenging for China nowadays. The strategic competition between China and the US is, in our view, more complex and multifaceted than the trade dispute between Japan and the US in the 1990s. In recent years, technology decoupling from the US has replaced the tariff war to become the major challenge for China. Beyond the bilateral relationship with the US, the globalization process has slowed down notably after 2008 (when the share of global trade as % of global GDP peaked), in sharp contrast to the golden days of globalization in the 1990s. The Russia-Ukraine war in 2022 further accelerated global supply chain relocation, which weighs on China’s potential growth.

Moreover, the room of macro policy stimulus is more limited in China nowadays than Japan in early 1990s. On the fiscal side, government debt was 61.9% of GDP in Japan in 1991, the start of the housing bust. Government debt rose to 131% of GDP by 2000 in Japan. In China’s case, although central government debt was only 20% of GDP, if adding local government debt and LGFV debt, total public debt reached 95% of GDP by end-2022.

Here’s the chart showing that:

As a result, JPMorgan warns that “the room for fiscal stimulus for China in the next 10 years is much smaller than Japan in the 1990s”. Nor do its economists think that China has any more scope to combat the economic miasma with monetary policy.

Similarly, on the monetary policy front, the BOJ’s policy rate was 8.1% in January 1991. The BOJ moved quickly after the housing bubble burst: by end-1993, the policy rate was cut to 2.4%; and in 1999, the BOJ became the first central bank to adopt zero interest rate policy. By comparison, China’s policy rate (7-day reverse repo rate) is already as low as 1.9%. The room for policy rate cuts for the PBOC, if deemed necessary, is much smaller than the BOJ in early 1990s.

What’s the diagnosis, doc?

So why then does JPMorgan think that China isn’t about to suffer a Japan-style long-term balance sheet recession? It boils to the differences between “ordinary” economic downturns and Koo’s diagnosis of Japan’s pretty unique travails.

When asset prices fall, firms face binding borrowing constraints with balance sheet deteriorating, forced asset sales can further push asset prices lower and form a self-reinforcing downward spiral between asset prices and economic activities. In other words, asset price decline is critical in understanding the phenomenon of balance sheet recession.

Following this argument, balance sheet recession is not a reality yet in China. The Chinese government has adopted the strategy of protecting house prices but letting volumes correct dramatically. This is in sharp contrast to the Japan’s episode, when prices and volume fell simultaneously. As a consequence, the macro cost (sharp decline in volume activity and slower real estate investment) is larger in China, but the benefit is that financial risk associated with asset price decline has stayed under control.

Also Japan’s balance sheet recession manifested itself in a huge deleveraging by households and companies, but a massive increase in the government’s debt burden.

Corporate debt fell from the peak of 144.9 per cent of Japan’s GDP in 1993 to 99.4 per cent in 2004, and household fell from 71 per cent in 1999 to 60 per cent in 2007, even as government debt ballooned, pushing the overall burden for the economy as a whole higher.

In contrast, China’s debts have been building up across the board with hardly any interruptions since 2008, and this is likely to continue, according to JPMorgan.

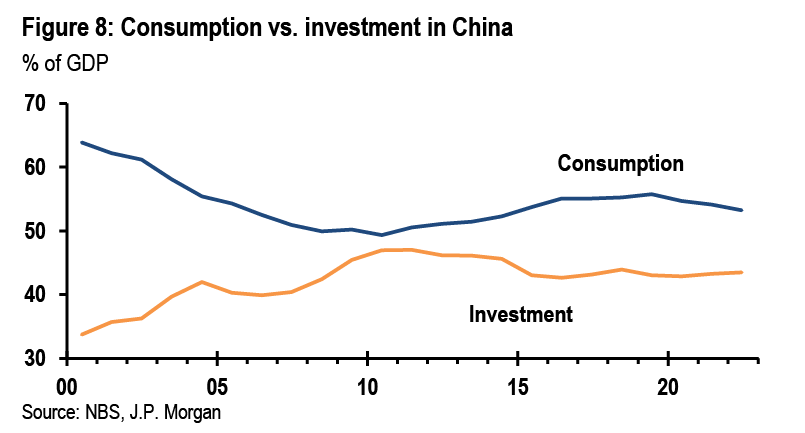

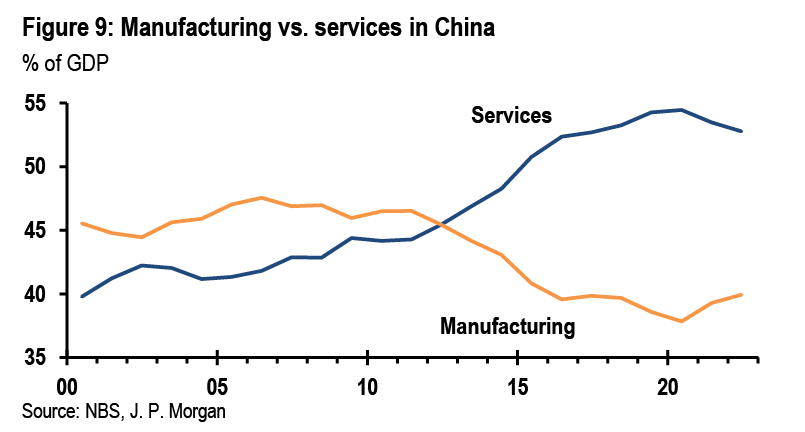

First, China’s economic structure has been characterized by high investment, and high savings. The much larger share of investment (vs. consumption) and manufacturing (vs. services) than other economies implies that the Chinese economy is more credit-driven, i.e. naturally debt-driven.

Second, China’s financial market has been dominated by indirect financing (via bank loans), and bond financing has risen faster than equity financing in recent years in capital market developments. This also leads to continuous debt increase. In order to slow down the pace of debt increase, the government will need to push forward capital market development (especially equity market, PE/VC, etc.) and the transformation of economic structure from high credit-intensify to low credit-intensity sectors.

This means a policy shift from investment to consumption, and equal support for upgrading of both services and manufacturing sectors. There were encouraging changes in China’s economic structure in the past decade, but the trend has somewhat been reversed in recent years.

Here are some charts showing that shift (zoomable chart 1 and zoomable chart 2):

{kind=link}

{kind=link}

But the fact that Chinese debts have continued to rise and are likely to do so for the next few years — and that the property market hasn’t imploded yet — is not really an argument against China’s Japanification. Indeed, it might only indicate that a full-scale version just hasn’t started yet.

Moreover, no economic crisis is ever going to be identical. Of course China will not follow Japan’s economic trajectory perfectly, or even vaguely. They’re very different countries, and these are very different times.

But there are enough broad similarities to think that the overall disease — a protracted period of declining demographics, economic sluggishness, deleveraging and deflationary pressures that defies fitful government efforts to dispel the miasma — might end up being pretty similar.